The backdoor Roth IRA is an invaluable tax-planning tool for high-income individuals who want to maximize their tax-advantaged retirement savings. While direct Roth IRA contributions are restricted once your modified adjusted gross income (MAGI) exceeds certain limits ($144,000 for single filers and $214,000 for married filing jointly in 2026), the backdoor Roth provides a legal workaround.

The Mechanics

The basic mechanics are straightforward: First, you make a contribution to a traditional IRA, which has no income limits. Then, you convert those funds to a Roth IRA, triggering a taxable event in the year of conversion. This creates tax-free growth and withdrawals in retirement, rather than the tax-deferred treatment of a traditional IRA.

However, the details require careful consideration. Any pre-tax money converted is taxed as ordinary income, which could push you into a higher marginal tax bracket and potentially trigger increases in your Medicare Part B and Part D premiums through the Income-Related Monthly Adjustment Amount (IRMAA). Ongoing tax planning is essential to navigate these nuances and optimize the timing of your Roth conversions.

Another important factor is your future income projections. If you expect your taxable income to be lower in the year of conversion compared to retirement, the backdoor Roth may be particularly advantageous. Conversely, if you anticipate higher income in the conversion year, it may be better to forgo the Roth conversion and instead focus on maximizing contributions to tax-deferred accounts like a 401(k) or traditional IRA.

The impact of Required Minimum Distributions (RMDs) from traditional retirement accounts should also be considered. Roth IRA conversions can help mitigate the tax burden of RMDs in retirement, which begin at age 73. By strategically converting funds to a Roth IRA over time, you can create a pool of tax-free retirement assets to complement your taxable and tax-deferred accounts.

Additional Considerations

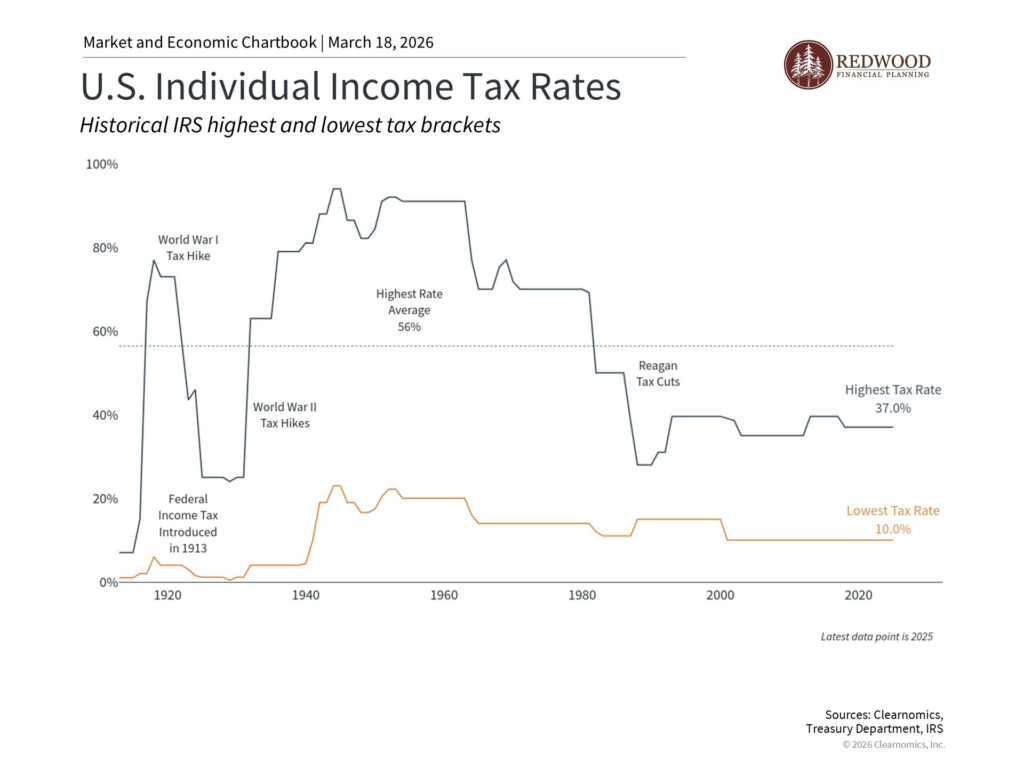

Tax Rate Dynamics

The current individual tax rate structure is an important factor in determining the optimal timing for Roth conversions. As shown in the provided chart, tax rates are currently at relatively low levels compared to historical norms. If you expect your future tax rate in retirement to be higher than your current rate, accelerating Roth conversions now may be advantageous. Conversely, if you anticipate a lower tax rate in retirement, it may make more sense to focus on tax-deferred savings in the present.

2026 tax brackets

| Tax rate | Single filers | Married couples filing jointly | Married couples filing separately | Head of household |

|---|---|---|---|---|

| 10% | $12,400 or less | $24,800 or less | $12,400 or less | $17,700 or less |

| 12% | $12,401 to $50,400 | $24,801 to $100,800 | $12,401 to $50,400 | $17,701 to $67,450 |

| 22% | $50,401 to $105,700 | $100,801 to $211,400 | $50,401 to $105,700 | $67,451 to $105,700 |

| 24% | $105,701 to $201,775 | $211,401 to $403,550 | $105,701 to $201,775 | $105,701 to $201,750 |

| 32% | $201,776 to $256,225 | $403,551 to $512,450 | $201,776 to $256,225 | $201,751 to $256,200 |

| 35% | $256,226 to $640,600 | $512,451 to $768,700 | $256,226 to $384,350 | $256,201 to $640,600 |

| 37% | Over $640,600 | Over $768,700 | Over $384,350 | Over $640,600 |

The marginal tax rates shown are important in the context of the backdoor Roth IRA strategy, as the tax liability incurred during the Roth conversion process is based on your ordinary income tax rate. Carefully considering your current and anticipated future tax bracket can help you determine the optimal timing and amount for Roth conversions.

For high-income earners, the ability to contribute directly to a Roth IRA phases out at modified adjusted gross income (MAGI) levels of $144,000 for single filers and $214,000 for married filing jointly in 2026. The backdoor Roth IRA allows these individuals to still access the tax-free growth and withdrawals of a Roth account, but the conversion process must be managed thoughtfully to minimize the tax impact.

Estate Planning Considerations

For high-net-worth individuals, the Roth IRA can be a valuable estate planning tool. Unlike traditional IRAs, Roth IRAs are not subject to Required Minimum Distributions (RMDs) during the account owner’s lifetime. This allows the assets to continue growing tax-free and potentially be passed on to heirs in a more tax-efficient manner.

Coordination with Other Retirement Accounts

The backdoor Roth IRA strategy should be considered in the context of your overall retirement savings, including employer-sponsored plans like 401(k)s and 403(b)s. Maximizing contributions to these accounts, especially if they offer employer matching, can further enhance your long-term financial security.

Ongoing Monitoring and Adjustments

Given the complexity of the backdoor Roth IRA strategy and the potential for changes in tax laws, it’s crucial to maintain an ongoing dialogue with your tax and financial professionals. Regularly reviewing your plan, adjusting contributions and conversions as needed, and staying informed of legislative updates can help you capitalize on this powerful tool while mitigating potential pitfalls.

By carefully navigating the nuances of the backdoor Roth IRA, high-income earners can unlock significant long-term tax savings and better position themselves for a financially secure retirement.

Ultimately, the decision to utilize the backdoor Roth IRA strategy should be made within the broader context of your overall financial plan and retirement income goals. Factors such as your current and projected tax rates, investment time horizon, and estate planning objectives all play a role in determining the optimal approach.