You’ve probably heard some version of this advice: “Wait until 70 to claim Social Security. You’ll get the biggest check.”

Mathematically, that’s true. But real life doesn’t follow spreadsheet logic.

The idea that waiting is always better has become something of a modern retirement mantra. But in the real world, where health, lifestyle, longevity, and personal values come into play, the “best” strategy isn’t always the one with the highest monthly benefit.

Here are three reasons why claiming Social Security early can be a strategic move:

1) Retirement isn’t only about income. It’s about timing.

According to the Social Security Administration, nearly a quarter of eligible Americans claim at 62, the earliest possible age. That choice is often about psychology and priorities, not just need. If your health is uncertain, if your plan includes front-loaded travel and experiences, or if you simply value spending more while you feel your best, starting sooner can turn “paper alpha” into “life alpha.” Money is a tool, not a scorecard. A smaller, earlier check that funds peak-energy years may deliver more life satisfaction than a larger check later. This also respects behavioral reality: people discount the future. Building some immediate reward into the plan keeps retirees engaged and compliant with the rest of the strategy.

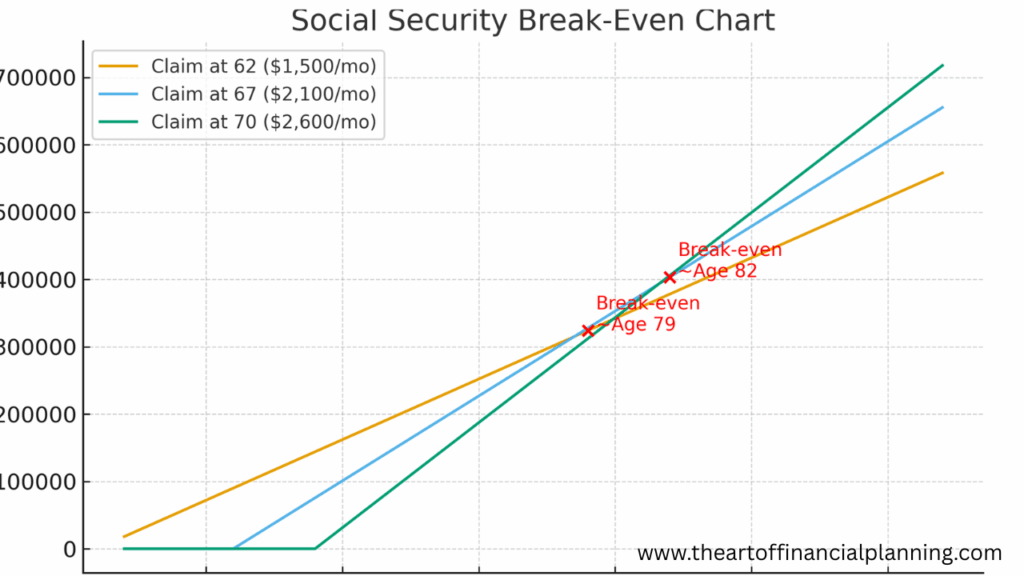

2) The break-even point is only part of the picture.

Yes, delaying can increase benefits roughly 8% per year past full retirement age, and the lifetime “win” shows up if you live long enough. But break-even charts quietly assume:

- You won’t need to tap your portfolio to cover the income gap.

- Markets cooperate while you’re waiting.

- You’ll actually want to spend the same—or more—later.

In practice, claiming earlier can reduce sequence-of-returns risk by lowering withdrawals in the first 5–8 years of retirement. For a retiree with a concentrated stock allocation or limited guaranteed income, turning on Social Security earlier may protect principal during down markets. It can also improve peace of mind—an underappreciated outcome that often leads to better spending discipline and fewer panic-driven portfolio moves.

3) Your Social Security strategy should reflect your big-picture goals.

Claiming doesn’t happen in a vacuum. It touches taxes, healthcare, and portfolio longevity:

- Tax planning: Earlier benefits might allow smaller, steadier withdrawals—potentially keeping you in a lower marginal bracket. Alternatively, delaying benefits can create a Roth conversion window in your 60s. Either path can be “right” depending on goals and balances.

- IRMAA/Medicare: Higher income from RMDs + delayed benefits can trigger Medicare premium surcharges. Sometimes starting benefits earlier smooths modified adjusted gross income over time and avoids bracket creep.

- Survivor planning: For married couples, optimizing the higher earner’s benefit (often by delaying that benefit) can boost the survivor benefit for decades. That doesn’t mean both spouses must delay. A common approach: lower-earning spouse claims earlier for cash flow, higher-earning spouse delays to age 70 to maximize the survivor benefit.

- Portfolio pressure: If your required withdrawal to bridge to 70 is 6–7% of the portfolio, delaying may be riskier than it looks. If it’s 1–2% and markets are favorable, delaying might be attractive. Context rules.

How to decide?

- Health and longevity outlook: Family history, current health, and lifestyle habits matter. A realistic estimate beats a generic rule.

- Income gap math: What’s the withdrawal rate needed if you wait? What’s the impact in a bear market?

- Tax map: Model 10–15 years of cash flows, showing brackets, IRMAA thresholds, RMDs, and Roth opportunities. Let taxes inform timing.

- Household strategy: Coordinate spousal benefits and survivor needs, not just individual maximization.

- Values and timing: Identify “peak-experience” years and fund them deliberately. If the dream is a 6-week European trip at 64, the plan should reflect it.

A better question

The question isn’t “How do I get the most from Social Security?” The better question is “How does Social Security support the retirement I actually want?” For some, that means waiting until 70. For others, it means claiming earlier to protect the portfolio, smooth taxes, fund meaningful experiences, or reduce stress.

The “wait until 70” rule is neat, simple, and easy to repeat. But your life isn’t neat or simple—and your plan shouldn’t be either. The right claiming strategy is the one that funds your best years, protects your downside, and aligns with your values, taxes, health, and household dynamics. Sometimes that means delaying. Sometimes it means turning benefits on sooner to reduce sequence risk, smooth taxes, or simply buy back time while you feel your best.

You don’t have to guess. Model a few realistic paths, pressure-test them, and choose the option that gives you both enough income and enough confidence to actually live your plan. Maximizing a check is optional. Maximizing your life is the goal.