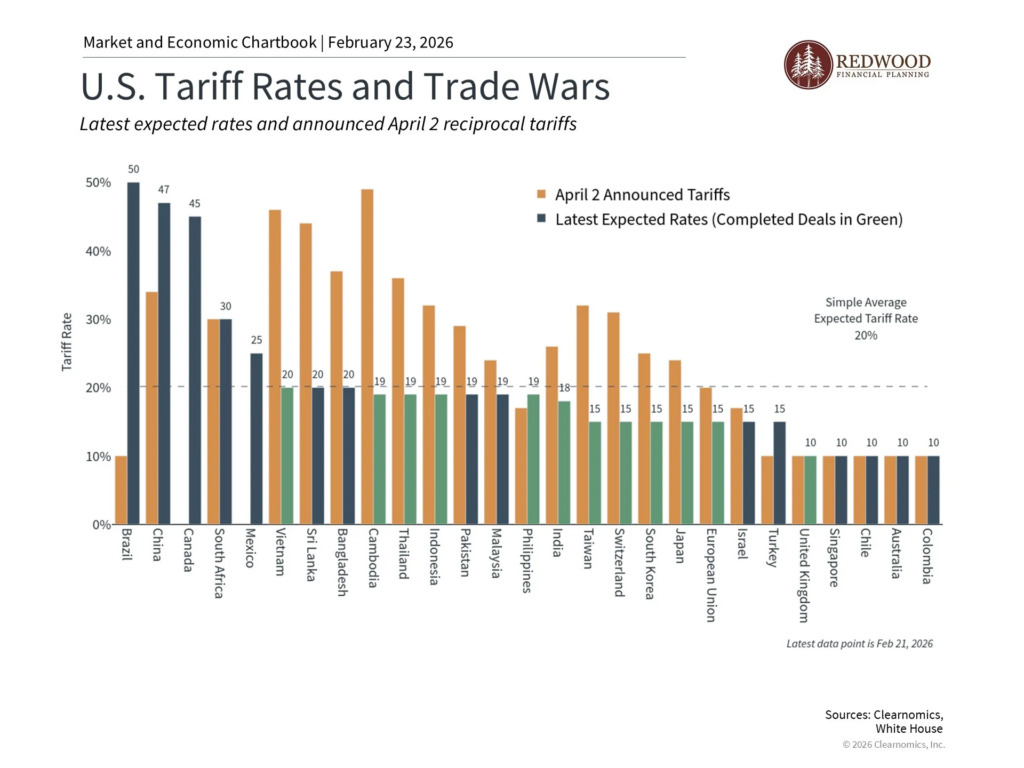

How does the Supreme Court’s tariff ruling affect the economy?

Here are the key facts:

• On February 20, 2026, the Supreme Court ruled 6-3 that the broad tariffs enacted by the White House under the International Emergency Economic Powers Act (IEEPA) were illegal. This matters for investors because trade policy has been a major source of market volatility and has affected all parts of the economy.

• The ruling struck down tariffs on virtually every country tied to trade deficits, as well as those on Mexico, Canada, and China over fentanyl concerns, though smaller tariffs on steel, aluminum, and cars remain in place. This includes the “reciprocal tariffs” that were announced during last April’s “liberation day.”

• It’s unclear whether refunds will be provided and how they will be enacted. Thousands of businesses were part of the lawsuits that made their way to the Supreme Court, so this could impact many sectors. According to data from U.S. Customs and Border Protection, roughly $90 billion of the approximately $195 billion in tariffs collected under IEEPA may need to be refunded.

• The White House may attempt to re-enact tariffs under other legal frameworks, though those laws have procedural limits and may not allow tariffs as sweeping as the ones struck down. So, while this minimizes one tool the administration has been using for international negotiations, they may still be able to implement tariffs in other ways.

The included chart shows the level of import tariffs across different countries. These tariffs have led to short-term volatility, but the market has remained resilient over the past year.

While policy changes like this can create short-term uncertainty, it is worth remembering that corporate earnings, economic growth, and valuations tend to be the true drivers of long-term market performance.

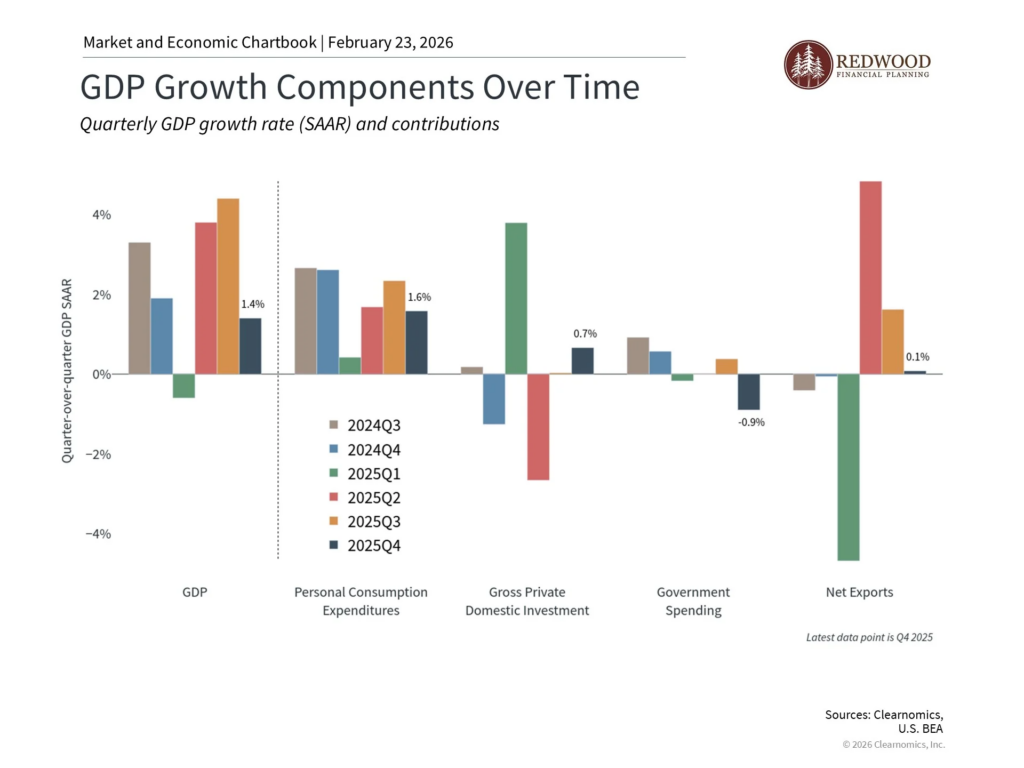

Why did GDP weaken last quarter?

Here are some key factors to consider:

• The latest report by the Bureau of Economic Analysis shows that real GDP grew at a 1.4% annual rate in the fourth quarter of 2025. This is below the 2.8% economists had expected and a significant step down from the 4.4% growth in the third quarter.

• This deceleration was primarily due to government spending and trade. The domestic economy, which is measured by a calculation called “real final sales to private domestic purchasers,” increased 2.4% in Q4. This means that consumer spending and business investment were quite healthy.

• Federal government spending fell at a 16.6% rate, subtracting nearly 1.2 percentage points from GDP, largely due to the government shutdown from October to mid-November 2025. Meanwhile, net exports contributed very little to GDP after adding to growth in Q2 and Q3 last year.

• Economists are concerned about a “K-shaped” economy in which some experience growth while others are struggling. This can be seen in the divergence between corporate profits and broad economic growth, versus the slowing job market and poor consumer sentiment.

The included chart shows recent GDP components, helping to illustrate how government spending, consumer activity, and trade each contributed to last quarter’s results.

While short-term GDP data can raise questions, the broader trend of steady consumer spending and business investment is a reminder that long-term investors are best served by focusing on the overall trajectory of the economy rather than any single quarter.

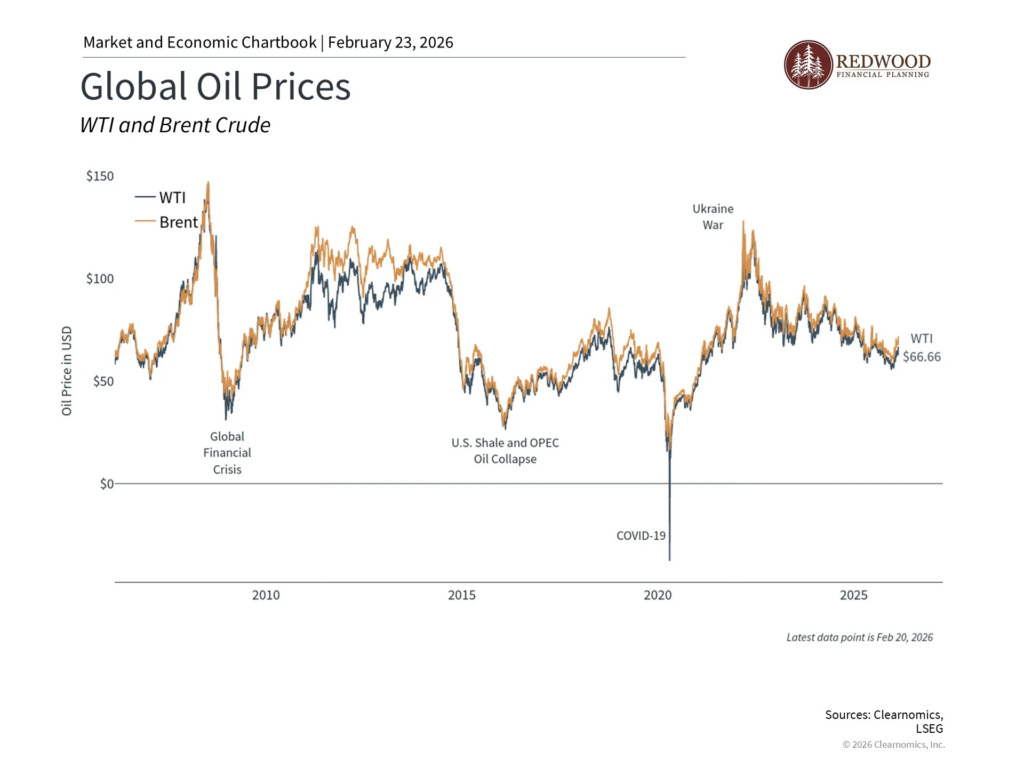

What are the market risks of a possible escalation with Iran?

Here are some key points to consider:

• Tensions between the U.S. and Iran have escalated, with the Trump administration deploying F-35 and F-22 fighters, a second aircraft carrier, and air defenses to the Middle East. The U.S. is demanding an end to Iran’s nuclear enrichment program and constraints on its ballistic-missile program. President Trump has signaled that the U.S. would decide its next move by early March if Iran does not agree to a nuclear deal.

• Energy markets have begun to react, with Brent crude and West Texas Intermediate both rising. This year, oil prices have risen approximately $10 per barrel, with Brent crude jumping from $60 per barrel to around $70. However, it’s important to keep in mind that these prices are still low by historical standards.

• A key risk is whether any conflict could threaten the Strait of Hormuz, a critical waterway carrying roughly one-third of the world’s oil supply. A disruption there could send oil prices significantly higher and add to inflationary pressures globally. This has been a concern over the past several years as Middle East tensions have flared.

• Geopolitical risks are an unavoidable fact of investing. Historically, market and economic indicators have generally recovered from geopolitical volatility once the initial situation passes. This was true earlier this year when the U.S. conducted operations in Venezuela as well.

The included chart on oil prices provides helpful context on how markets have historically responded to major world events. While events like Russia’s invasion of Ukraine and the Hamas attack on Israel caused short-term volatility, oil prices have remained fairly stable over the past few years.

While geopolitical events can cause short-term market turbulence, history consistently reminds us that staying patient and focused on long-term financial goals has generally been the most rewarding approach for investors navigating uncertain times.

With so many questions—it is important to maintain a long term perspective but still be informed of current events.