Looking ahead at a home purchase?

High rates convincing you to stay put as long as possible?

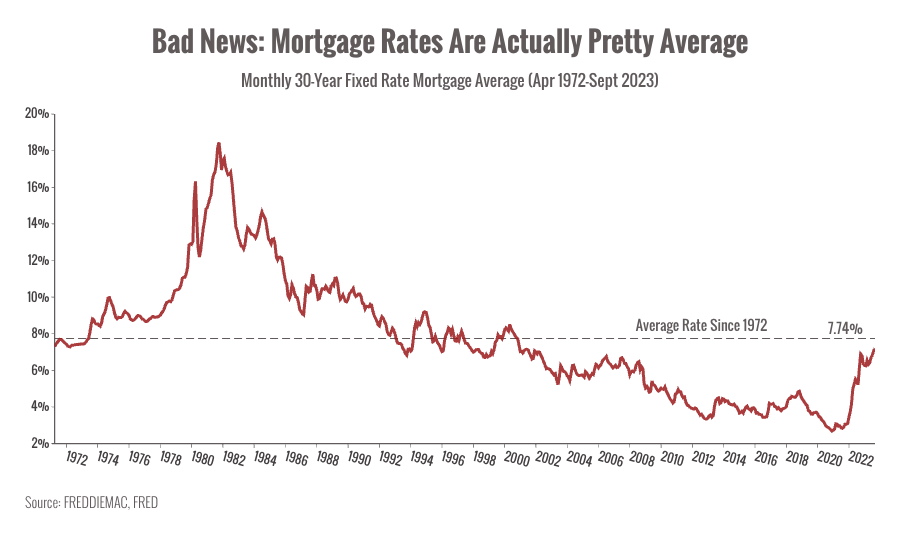

With mortgage rates pushing above 7% again, you might think a reasonable mortgage is out of reach.

I’ve got some not-so-great news for you. Current rates aren’t actually that high, historically speaking.

They just look high because we’ve gotten used to low rates over the last few decades.

|

But here’s some good news:

You actually have more leverage as a buyer than you might think.

The reality is that many lenders and home sellers are losing deals as buyers get cold feet.

They’re increasingly willing to find creative ways to get your business.

Those pressures could work in your favor.

Here are three tips on finding a decent mortgage in a high-rate environment.

#1 ALWAYS ALWAYS ALWAYS shop around for your mortgage

While it’s common for real estate firms to push you toward a lender they know and like to work with, mortgage rates can vary tremendously by lender.

That “dispersion” of rates for the same borrower means getting multiple quotes and comparing the total cost of the loan can save you thousands.

One study found that borrowers who compared at least four rate quotes could have saved more than $1,200 each year.1

A quick way to compare loans is to look at the loan’s annual percentage rate (APR).

If two loans offer the same interest rate, but one has a higher APR, that means higher costs are baked into the details.

#2 Ask lenders to reduce or eliminate fees

Once you’ve picked a lender or two, take a look at the loan estimates and look for opportunities to negotiate.

You can even ask lenders to beat their competitors’ offers if you get everything in writing.

If you already have a relationship with a lender, you can sometimes leverage customer loyalty to try for a better deal.

In some cases, you can even ask the lender to add a no-cost refinance in the future, so feel free to negotiate beyond what’s already in the estimate.

#3 Ask sellers for closing credits or a rate buy-down

Closing costs can add a lot to your home purchase, so asking sellers for help covering those fees can make a big difference to your out-of-pocket costs.

In some cases, you might find sellers and homebuilders willing to offer a rate buy-down, in which they help you temporarily or permanently lower your mortgage rate.

A temporary buy-down allows you to temporarily pay a lower interest rate for the first few years of the mortgage.

A permanent buy-down allows you to permanently lower your interest rate across the life of the loan.

One note: A permanent buy-down would look less attractive if rates fall in the future, so it’s wise to compare your options and understand the tradeoffs.

Mortgage rates will likely remain high, so becoming a savvy negotiator can help save you thousands.